PMS vs Mutual Funds: Why HNIs Hit a Glass Ceiling at ₹50 Lakhs

Table of Contents:

Click to Expand

- The Dream of the "Successful" Mutual Fund Portfolio

- The ₹50 Lakh Glass Ceiling: When Diversification Becomes Dilution

- The Hidden HNI Tax Trap in Mutual Funds

- The PMS Advantage: Hyper-Customization & Direct Ownership

- The "2+20" Fee Fallacy: Why You Should Want to Pay for Alpha

- The Vestbox Research: Dismantling a Bloated Mutual Fund Portfolio

- The Next Step: Which Institutional Structure Actually Fits You?

For a first-time investor putting ₹5,000 a month into a Nifty 50 Index fund, mutual funds are the greatest financial invention in human history. They offer instant diversification, zero effort, and compounding magic.

However, as your wealth grows, your financial needs evolve. The very mechanisms that make mutual funds incredibly safe and accessible for the masses can begin to act as structural friction points for high-net-worth individuals (HNIs).

Once your corpus crosses the ₹50 Lakh mark, you hit what wealth managers call the "Glass Ceiling." If you want to break through it, you must explore Portfolio Management Services (PMS).

Here is the mathematical reality behind why HNIs eventually outgrow mutual funds, and why PMS becomes a logical next step, not just a luxury status symbol.

The Dream of the "Successful" Mutual Fund Portfolio

Log in to any standard mutual fund app and look at your statement. If you’ve been investing for a few years, you likely see a positive overall return.

You feel successful. The app flashes green numbers, and you believe your wealth is compounding efficiently.

In reality, this success is largely a reflection of the broader market's momentum. When you strip away the market's rise and isolate your actual portfolio architecture, you may find overlapping funds, hidden commissions through Regular plans, and concentrated sectoral risks you didn't intentionally take.

The mutual fund structure naturally aggregates your money with millions of others. You don't see the overlapping stocks; you see a single NAV number. Once your wealth crosses a certain threshold, this lack of granular transparency stops being a minor annoyance and becomes a massive financial liability. That is exactly where the Glass Ceiling begins.

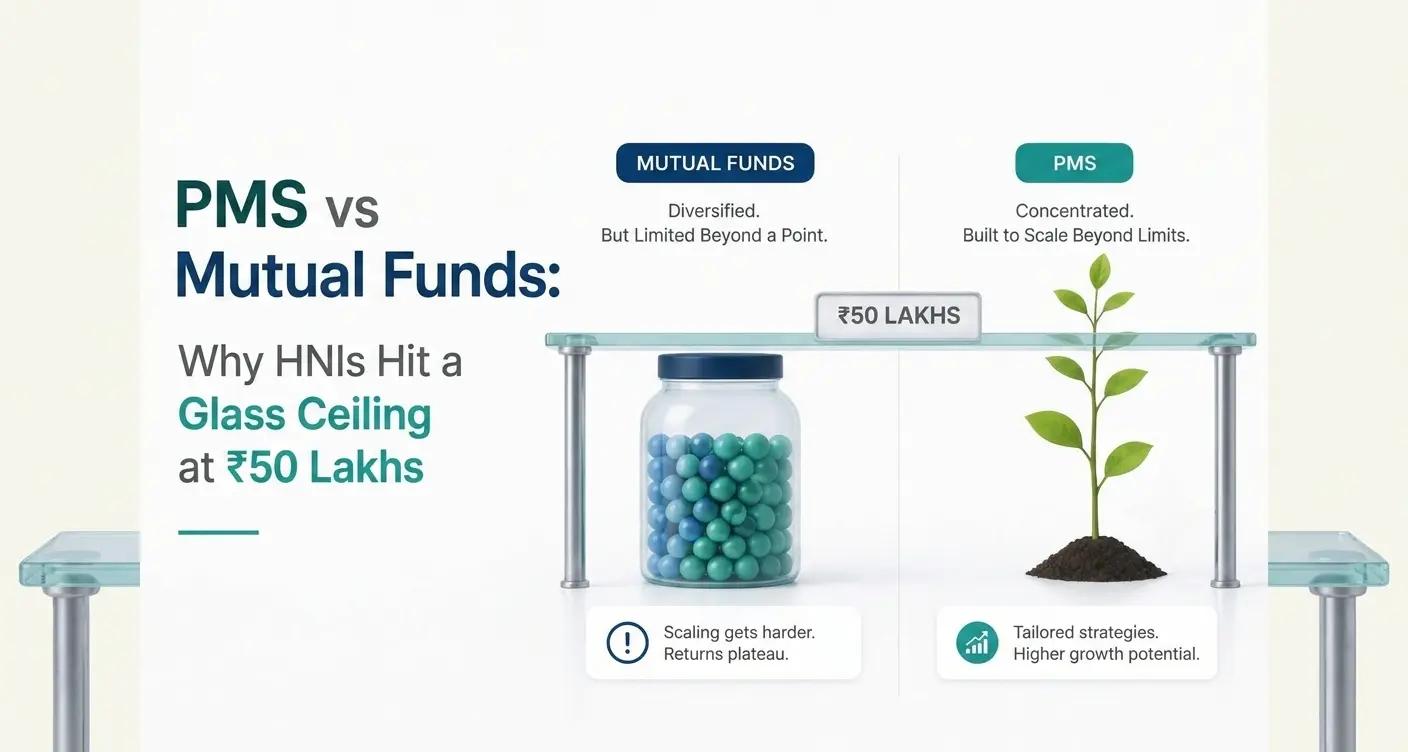

The ₹50 Lakh Glass Ceiling: When Diversification Becomes Dilution

In the retail world, everyone preaches diversification. "Don't put all your eggs in one basket." This is a brilliant rule for beginners. But in the HNI world, over-diversification is a guaranteed way to dilute your returns. Standard SEBI equity mutual funds are mandated to hold anywhere from 50 to 100+ stocks.

Let’s say you accumulate ₹1 Crore across four top-rated mutual funds. Because of overlapping mandates (as we exposed in the Diworsification guide), your underlying portfolio likely holds 120+ stocks.

You now effectively own ₹80,000 worth of Reliance, ₹65,000 worth of HDFC Bank, and ₹40,000 worth of a mid-cap chemical company.

You are no longer an active investor; you have unintentionally become a micro-index fund paying active management fees. When a mutual fund holds 100 stocks, its returns are mathematically handcuffed to the broader market. The fund manager cannot generate outsized returns because their best ideas are diluted by 90 mediocre stocks required to meet broad "diversification norms."

The Hidden HNI Tax Trap in Mutual Funds

This is a structural limitation that affects tax optimization and costs HNIs crores over a decade.

When you invest in a mutual fund, you do not own the underlying stocks. You own "units" of a trust. This creates a limitation during tax-loss harvesting.

The Mutual Fund Structure: If the market crashes and your mutual fund drops 20%, you cannot tell the fund manager, "Sell my specific loss-making stocks so I can offset my capital gains tax this year." The fund manager makes decisions for the entire pool. If they don't sell, you lose out on the tax benefit. Even if they do sell, the tax benefit is trapped within the mutual fund structure, rather than offsetting your personal capital gains from direct equity or real estate.

The PMS Solution: Under SEBI PMS regulations, a Portfolio Management Service holds stocks directly in your personal Demat account. You are the legal owner of the shares.

If you have a ₹50 Lakh PMS portfolio and the market declines, your dedicated portfolio manager can execute targeted tax-loss harvesting specifically for you. They can sell losing stocks to offset the capital gains you realized when you sold a physical property or direct shares that year. This kind of personalized tax optimization is often enough to make the fee for a PMS worth it for high-net-worth individuals in the highest tax brackets.

The PMS Advantage: Hyper-Customization & Direct Ownership

When you cross the ₹50 Lakh threshold, your financial life becomes complicated. You have ESOPs, equity investments, real estate, and fluctuating liquidity requirements. A pooled solution like a mutual fund cannot adapt to your specific life situation.

1. Concentrated Alpha: A PMS manager typically holds only 15 to 25 high-conviction stocks. If their research says a specific company will double in three years, they don't have to buy 50 other stocks to dilute the impact. They allocate 8% of your portfolio to it. If they are right, it massively moves the needle on your ₹1 Crore.

2. Exit Load Freedom: Mutual funds often carry a 1% exit load if you withdraw before 12 months to discourage short-term trading. PMS has no exit loads. You have a family emergency and need ₹15 Lakhs tomorrow? The manager sells the most liquid stocks in your portfolio, and the money hits your bank account in T+1 days. No penalties.

3. Exclusion Mandates: You work in the IT sector, so you own ESOPs in IT companies. You can explicitly mandate your PMS manager: "Do not buy any IT stocks to avoid concentration risk." A mutual fund manager cannot do this if IT is outperforming, as their mandate is to maximize returns for the pool.

The "2+20" Fee Fallacy: Why You Should Want to Pay for Alpha

The biggest objection to PMS is the fee structure: typically a 2% fixed management fee plus a 20% profit-sharing fee (on gains above a hurdle rate, like a 10% benchmark).

HNIs look at 20% and get furious. "Why should I give away a fifth of my profits?"

Let’s flip the perspective. If a mutual fund generates 12% and charges 1.5%, your net is 10.5%. If a PMS generates 18% through concentrated bets, charges a 2% fixed fee, and takes 20% of the 8% profit above the 10% benchmark, your net return is roughly 15.4%.

You didn't lose 20% of your money. You paid 2.6% for institutional-grade, customized alpha, and you still walked away with 4.9% more money in your pocket than the mutual fund investor. You aren't paying for the fee; you are paying for the intellectual edge of a dedicated analyst whose sole job is to grow your specific Demat account.

The Vestbox Research: Dismantling a Bloated Mutual Fund Portfolio

A tech executive came to Vestbox with ₹1.5 Crore spread across 9 mutual funds on three platforms.

The Problem: He was frustrated. His portfolio XIRR was stuck at 11%, barely beating the Nifty, despite holding "aggressive" mid and small-cap funds.

The Vestbox Audit: We ran his holdings through our diagnostic engine. The result? His top 10 stocks comprised 45% of his entire portfolio. He was essentially holding a highly expensive, replica Nifty index fund. Furthermore, he had massive unrealized gains trapped in funds he wanted to exit, but the 1% exit load was preventing him from rotating his capital.

The Execution: We ensured a gradual shift to a tailor-made PMS regime. We suggested deploying funds optimally, without incurring significant tax liabilities or any exit loads (waiting out the specific timelines where necessary).

The Result 18 Months Later (Expected): The PMS mandate, holding a concentrated basket of 22 high-conviction stocks with a clear exclusion mandate for its employer's sector, generated an XIRR of 19.2%. More importantly, the client utilized targeted tax-loss harvesting during a mid-year correction to offset ₹8 Lakhs in capital gains tax from his direct equity trades. The PMS didn't just make him wealthier; it acted as a personalized tax-planning tool.

The Next Step: Which Institutional Structure Actually Fits You?

Mutual funds are rigid, pooled vehicles designed to provide democratic access to the markets. PMS is a bespoke suit tailored for your specific tax bracket, risk appetite, and financial goals.

However, PMS is not the only way to access institutional strategies. As HNIs realize they need more than standard mutual funds, they usually discover three primary alternatives: SIFs (Specialized Investment Funds), AIFs (Alternative Investment Funds), and PMS.

They all operate differently. SIFs offer derivative hedging with lower barriers to entry. AIFs offer the most aggressive hedge-fund-like strategies but come with massive lock-ins. PMS offers direct ownership and hyper-customization.

If you want to see the exact structural differences, transparency levels, tax implications, and liquidity profiles of all four side by side, read our complete SIF vs PMS vs AIF vs Mutual Funds breakdown.

Stop forcing a square peg into a round hole. Once your wealth hits scale, generic products will only deliver generic returns. Demand a customized architecture.

Explore our complete guide: What is PMS? A Complete Guide to Portfolio Management Services in India. What is a Portfolio Review? A Complete Guide to Fixing Your Investments

Disclaimer

Mutual fund investments are subject to market risks. Read all scheme-related documents carefully. Please consult a certified financial advisor before making any investment decisions.

Trust & Compliance

This article has been created following our strict Editorial Policy. We believe in complete transparency regarding how we operate; you can read our Disclosures. For legal liabilities and risk factors, please review our Disclaimer.

Share & Save Article

Other Posts

What is Portfolio at Risk? A Complete Guide to Meaning, Formula, Calculation, & Benefits.

Jun 5, 2026

What is SIP & How Does It Actually Work?

May 27, 2026

What is an AMC in Mutual Funds? Understanding Asset Management Companies

May 27, 2026

How PMS Works: A Complete Guide to Construction, Monitoring, and Reporting

May 27, 2026