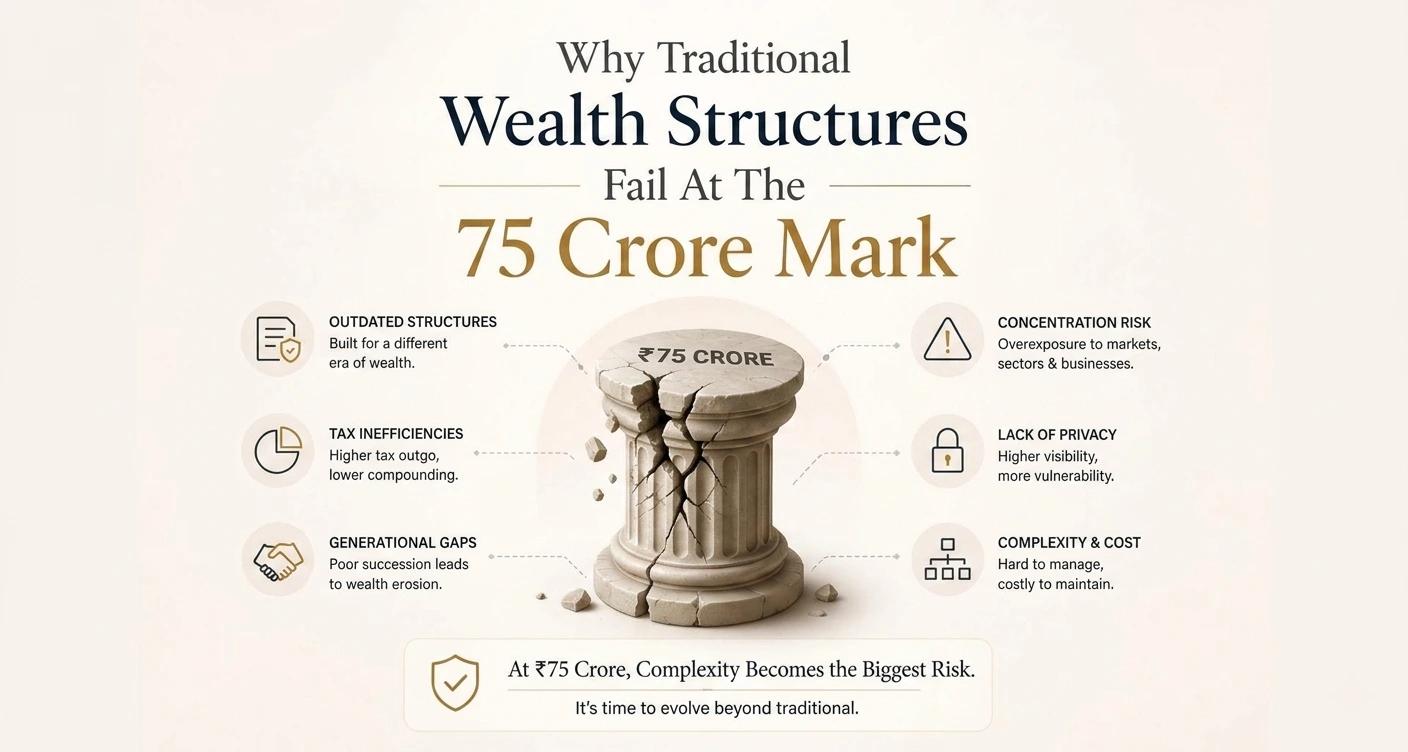

Why Traditional Wealth Structures Fail At The 75 Crore Mark

Table of Contents

Click to Expand

There is a pervasive illusion among newly minted ultra-high-net-worth individuals that wealth management scales linearly.

The thinking goes like this: If a collection of mutual funds and direct stocks worked brilliantly to accumulate the first ₹25 Crores, the logical next step is to inject the remaining ₹75 Crores into the same structure.

This is a dangerous miscalculation. The mechanisms that generate wealth during the accumulation phase actively destroy wealth during the preservation phase. When your capital crosses a critical threshold, typically around the ₹50-₹75 Crore mark, traditional retail structures break down under their own weight.

If your wealth has reached this inflection point, you must explore institutional wealth architectures before structural friction erodes your generational capital.

The Linear Scaling Fallacy

To understand why traditional wealth structure fails at scale, you must understand the difference between a retail investor and an institutional capital allocator.

A retail investor deploying ₹5 Lakhs a year is effectively a speedboat. They can move quickly, enter and exit mid-cap mutual funds, and their individual trades have zero impact on the broader market. The market is an ocean, and they barely create a ripple.

An individual deploying ₹75 Crores is an aircraft carrier. If they attempt to navigate using speedboat strategies, they will sink. At this scale, the physics of the market change entirely.

The Hidden Friction of Massive Liquidity

The most insidious destroyer of wealth at scale is market impact cost.

Imagine you decide to allocate ₹30 Crores into a top-performing mid-cap mutual fund. The fund currently holds ₹2,000 Crores in assets. Your single investment suddenly increases the fund's AUM by 1.5%.

Because the fund's mandate requires it to deploy this cash into mid-cap stocks, the fund manager is forced to buy stocks in a market where you, the investor, are the dominant source of demand. As the manager buys, the stock price artificially inflates before the order is filled.

You have essentially paid a premium to buy your own demand. This slippage is rarely visible on a standard factsheet, but it silently strips basis points off your wealth every time a large transaction occurs. Traditional mutual funds are not built to handle single-ticket institutional block trades.

The Pooled Vehicle Drag at Scale

When you invest in a mutual fund or a standard retail product, you forfeit direct ownership of the underlying securities. You own units of a trust. While this is perfectly acceptable during the wealth creation phase, it becomes a severe structural limitation during the preservation phase.

At ₹75 Crores, your primary objectives shift from pure aggression to tax optimization and bespoke risk management.

If you hold a retail pooled vehicle, you cannot dictate the underlying strategy to optimize for your specific tax liability. If the market crashes, you cannot selectively extract the heavily lossmaking stocks to offset the massive capital gains you might realize from selling your primary business. The fund manager must act in the interest of the collective pool, not your bespoke balance sheet.

You are paying management fees to an AMC to hold a customized, massive chunk of wealth inside a generic, unyielding box.

The Institutional Capital Shift

When wealth crosses the ₹75 Crore mark, the structure must undergo a fundamental redesign. You stop buying retail products, and you start building bespoke institutional structures.

This requires moving away from publicly traded retail vehicles and accessing private markets governed by frameworks such as the SEBI AIF regulations framework.

1. Private Equity and Venture Capital: Instead of buying a mid-cap mutual fund and accepting market volatility, institutional architecture allows you to invest directly into the private equity funds that are actually buying and restructuring those mid-cap companies. You bypass the public market entirely, capturing returns before the retail public is even aware of them.

2. Structured Credit and Alternative Debt: Instead of putting ₹20 Crores into a corporate bond fund generating an 8% return, a custom wealth structure invests in private credit funds that make loans to quality corporates for 14-16%, earning the differential interest spread that banks earn on their lending. Such a solution necessitates a complex legal structure and direct dealmaking, something retail products can’t do.

3. Global Diversification and Jurisdictional Arbitrage: For a big player, having all the wealth invested in Indian equities entails exposure to currency risk and single-geography economic cycles. Institutional structuring would leverage offshore structures to invest in global technology indexes, US government securities, and foreign property investments, enabling them to hedge against a domestic slowdown on their legacy.

The Vestbox Scenario: Engineering a 75 Crore Moat

An entrepreneurial family in its second generation came to Vestbox with ₹80 Crores in liquid wealth, allocated across large-cap mutual funds, fixed deposits, and stocks.

The structure was generating a respectable 11% average return. However, when we stress-tested the architecture, the flaws were glaring. The mutual fund portion was suffering from severe overlap and market impact costs. The fixed deposits were suffering from brutal tax drag, barely beating inflation.

We did not "advise them to buy better funds." We redesigned their operating system.

We structured a Family Trust to hold the assets, creating a multi-generational tax shield. We transitioned a portion of the mutual fund capital into a Category II AIF focused on structured credit, immediately boosting their post-tax yield by 400 basis points without increasing downside risk. We allocated a tranche to a global equity basket to neutralize domestic currency risk.

The gross return remained similar, but the net, post-tax, post-friction returns increased dramatically, while the structural risk was fundamentally de-risked.

Beyond Returns: The Mandate of Preservation

At ₹10 Crores, your mandate is growth. You take calculated risks to multiply your capital.

At ₹75 Crores, your mandate is preservation. You already have more money than you will ever spend. The objective is no longer to double the money; the objective is to ensure the money is structurally immune to inflation, taxation, litigation, and human error.

You cannot achieve this level of structural immunity by purchasing retail financial products off a shelf. It requires an institutional wealth architecture tailored specifically to the legal, tax, and psychological profile of your family.

Stop scaling a system that was built for accumulation. Begin engineering a structure designed for preservation.

Disclaimer

Mutual fund investments are subject to market risks. Read all scheme-related documents carefully. Please consult a certified financial advisor before making any investment decisions.

Trust & Compliance

This article has been created following our strict Editorial Policy. We believe in complete transparency regarding how we operate; you can read our Disclosures. For legal liabilities and risk factors, please review our Disclaimer.

Share & Save Article

Other Posts

What is Portfolio at Risk? A Complete Guide to Meaning, Formula, Calculation, & Benefits.

Jun 5, 2026

What is SIP & How Does It Actually Work?

May 27, 2026

What is an AMC in Mutual Funds? Understanding Asset Management Companies

May 27, 2026

How PMS Works: A Complete Guide to Construction, Monitoring, and Reporting

May 27, 2026