The Complexity of Selling A Business Versus Building One

Table of Contents

Click to Expand

There is a dangerous misconception in the entrepreneurial community. Founders believe that building a business from scratch to a ₹100 Crores valuation is the pinnacle of mental endurance.

It is not.

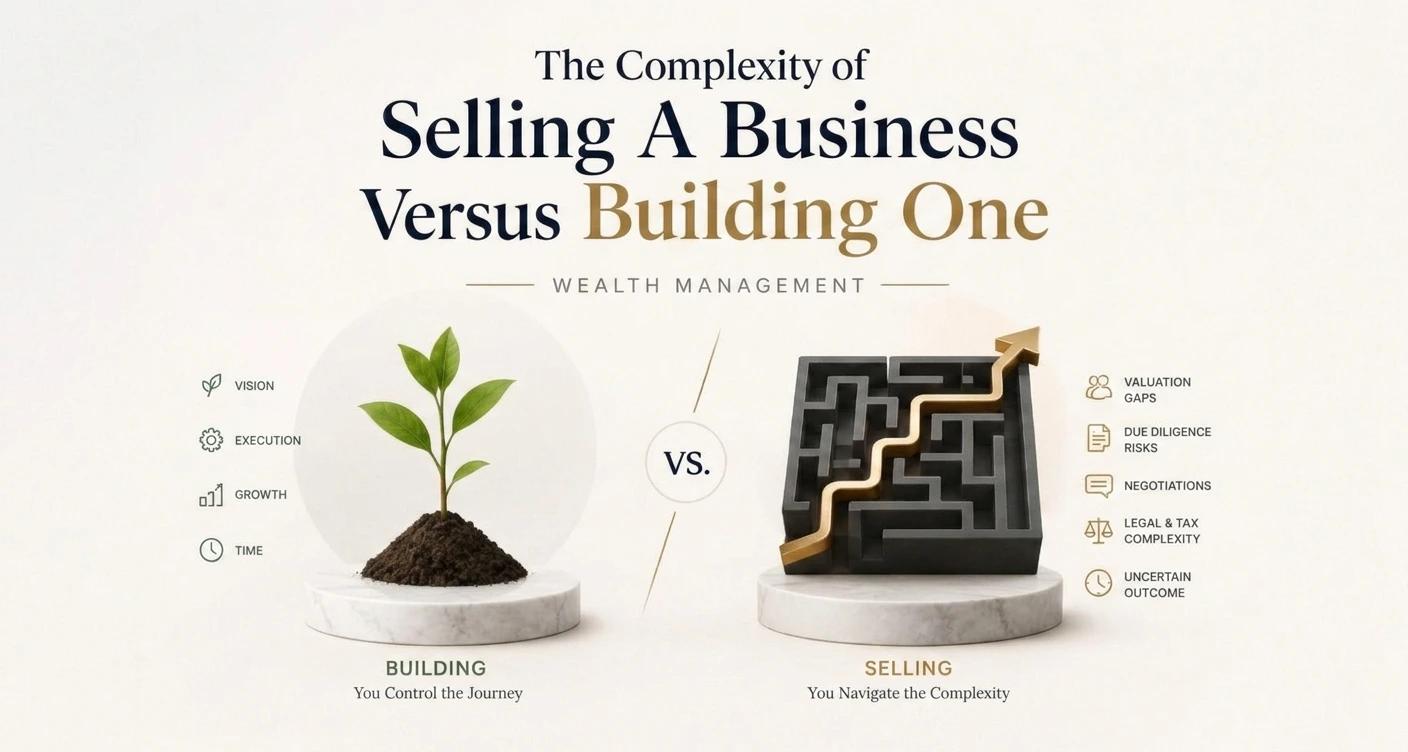

Building a business is an active, adrenaline-fueled sprint. You face enemies, pursue missions, and track daily metrics to validate your progress. You know exactly what to do next.

Selling that business for ₹100 Crores is where the real danger begins. You transition from an active operator to a passive capital allocator overnight. The wire hits your bank account, the celebration lasts a weekend, and then a paralyzing reality sets in. If you are navigating this exact transition, you must speak privately about wealth transition.

The Silence After the Wire

When you run a company, your wealth is trapped in the business. It is an illiquid asset, but it gives you a clear identity.

Once you sell, that identity vanishes. You are no longer the CEO of something. You are simply an individual holding a massive amount of liquid cash.

Founders often underestimate the psychological shock of this transition. Without the structure of a business to command their attention, they make the fatal mistake of treating their ₹100 Crore liquidity event like a standard retail investor manages a ₹10 Lakh bonus. They start buying commercial real estate they don't understand, taking meetings with private equity funds, or allowing traditional private bankers to peddle high-commission products.

The Paradox of Sudden Wealth

The fundamental paradox of sudden wealth is that the more money you have, the more complex the architecture required merely to preserve its purchasing power.

A ₹10 Crore corpus can be efficiently managed with a standard mix of mutual funds and direct equity. A ₹100-Crore corpus shatters traditional financial frameworks.

When you deploy capital at this scale, a 20% market drop is no longer your primary risk. The real dangers are structural: capital dilution, tax friction, and institutional roadblocks. Buying a standard large-cap mutual fund with ₹50 Crores creates massive market impact costs. You cannot just "set it and forget it." You need an entirely different operating system.

Why Retail Frameworks Fail at Scale

Traditional wealth management in India is built around product distribution. Banks and brokers are incentivized to allocate your capital into pre-packaged mutual funds, bonds, or insurance products that generate trailing commissions.

At a ₹100 Crores scale, these products become mathematically inefficient. You do not need a mutual fund wrapper; you need direct institutional access to Private Equity, bespoke debt instruments, global equities, and alternative assets.

Furthermore, standard retail frameworks are taxed inefficiently at scale. When you sell a business, the statutory capital gains framework becomes complex. Without preemptive structural planning, the sheer volume of taxation can severely impair your generational capital.

You cannot rely on a retail relationship manager to navigate this; you need a dedicated architectural desk.

The Taxation Labyrinth

We will not bore you with specific section numbers, as tax codes are fluid and context-dependent. However, the structural reality is absolute: a business liquidity event triggers massive capital gains obligations.

If a founder passively takes the cash, pays the tax, and tries to deploy the net amount, they have already permanently lost a portion of their life's work to the state.

Institutional wealth structuring involves creating legal envelopes such as specific trust structures guided by the Indian Trusts Act general framework before the transaction closes. It involves using legal avenues to defer, offset, or recharacterize tax liabilities so that the full weight of the capital can be deployed into compounding engines.

This cannot be done retroactively. It must be engineered in parallel with the business sale process.

The Isolation of the Founder

Perhaps the most underestimated risk in a liquidity event is social and psychological isolation.

As a founder, your peers were other founders. You spoke the same language of operations, hiring, and scaling.

Once you exit, you are suddenly surrounded by two dangerous groups: relatives who view you as a personal bank, and private bankers who view you as a commission target. You lose your trusted advisory network.

Founders often make catastrophic financial decisions in the first twelve months post-exit simply because they are lonely and lack a sounding board that understands the burden of ultra-high-net-worth capital. They make impulse investments in startup ecosystems or vanity real estate to feel the dopamine of "doing a deal" again.

The Institutional Architecture Required

Preserving a ₹100 Crore liquidity event requires building infrastructure that mirrors a sophisticated family office.

It requires a shift from "product picking" to "policy making." You need a documented family constitution. You need segregated buckets for liquidity, growth, and generational transition. You need an advisory desk that operates under a strict fiduciary standard, meaning it is legally bound to act in your best interests, free from hidden product quotas or conflicts of interest.

You spent two decades building a fortress around your business. When you sell the business, you must immediately build an equally rigorous fortress around the cash.

Do not let the complexity of sudden wealth silently erode what you spent a lifetime building.

Disclaimer

Mutual fund investments are subject to market risks. Read all scheme-related documents carefully. Please consult a certified financial advisor before making any investment decisions.

Trust & Compliance

This article has been created following our strict Editorial Policy. We believe in complete transparency regarding how we operate; you can read our Disclosures. For legal liabilities and risk factors, please review our Disclaimer.

Share & Save Article

Other Posts

What is Portfolio at Risk? A Complete Guide to Meaning, Formula, Calculation, & Benefits.

Jun 5, 2026

What is SIP & How Does It Actually Work?

May 27, 2026

What is an AMC in Mutual Funds? Understanding Asset Management Companies

May 27, 2026

How PMS Works: A Complete Guide to Construction, Monitoring, and Reporting

May 27, 2026