Flat ₹10k SIP vs. Step-Up SIP: The 10-Year Mathematical Proof

Table of Contents

Click to Expand

You get a promotion. Your salary increases by 15%.

What is the first thing you do? If you are like 90% of professionals, you upgrade your lifestyle. You move to a slightly better apartment, buy a newer phone, or start dining out more frequently.

This is known as "Lifestyle Creep." It is the silent killer of wealth creation. As your income grows linearly, your expenses grow proportionally, meaning your investment capacity stays the same.

If you want to see how much wealth you are leaving on the table by falling into this trap, run the step-up SIP calculation yourself to see the gap. The mathematical difference between a flat investment and a growing investment is one of the most violent wealth multipliers in finance.

The Lifestyle Creep Trap

Most investors set up a Systematic Investment Plan (SIP) when they are 25 or 27 years old. Let’s say they start with a comfortable ₹10,000 per month.

Five years later, their income has doubled. But their SIP is still ₹10,000.

They feel good because they have a "habit" of investing. But their money is working at the capacity of a 25-year-old, while their earning potential is now at a 30-year-old level. This creates a massive imbalance between their human capital (career) and their financial capital (investments).

The Fundamental Flaw in a Flat SIP

A flat ₹10,000 SIP relies entirely on the market to do 100% of the heavy lifting. You are relying on the 12% average annual return to compound your wealth.

But the stock market doesn't care that you got a promotion. The market’s compounding curve is fixed based on the principal you put in. If you don't increase your principal, your compounding curve flattens out relative to your actual earning power.

A Step-Up SIP fixes this flaw by aligning your investment growth with your income growth.

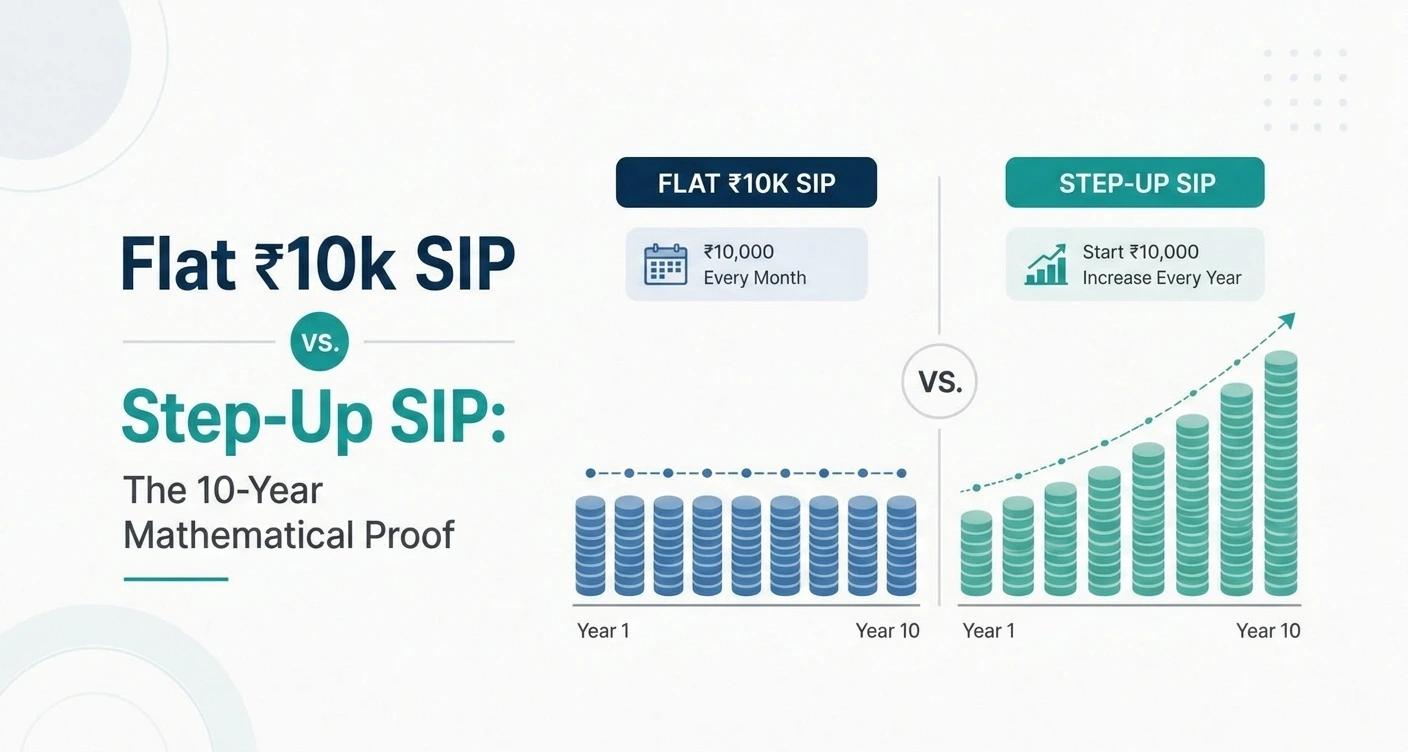

The 10-Year Calculation Proof

Let’s look at the exact numbers over a 10-year horizon, assuming a standard estimated return of 12% for a broad equity mutual fund under SEBI categorization of mutual funds.

Investor A (The Flatliner): Invests a strict ₹10,000 every single month for 10 years, regardless of appraisals.

- Total Invested: ₹12 Lakhs.

- Estimated Corpus: ₹23.2 Lakhs.

Investor B (The Step-Up): Starts with ₹10,000 and increases the SIP by just 10% annually to keep pace with inflation and salary increases. (Year 1: ₹10k, Year 2: ₹11k, Year 3: ₹12.1k, etc.)

- Total Invested: ₹19 Lakhs.

- Estimated Corpus: ₹32.6 Lakhs.

Look closely at the math. Investor B only put in ₹7 Lakhs more out of their pocket over a decade (less than ₹6,000 extra per month on average). But their final corpus is higher by ₹9.4 Lakhs.

You didn't have to take extra risk. You didn't have to pick a better mutual fund. You increased your input to match your real-world income trajectory, and the compounding engine did the rest.

The Vestbox Data: Automating Wealth Upgrades

The biggest argument against Step-Up SIPs is psychological: "I won't have the discipline to increase my SIP every year."

That is a valid human concern. That is why the smartest investors automate it.

A Vestbox client, a software engineer, set up a Top-Up SIP mandate linked to his primary mutual fund. He instructed the system to automatically increase his SIP by exactly 15% every April, to coincide with his annual appraisal cycle.

He never had to log in and make the decision. He never felt the "pain" of parting with extra money because the system debited it before he could spend it on lifestyle upgrades.

When we reviewed his portfolio after 8 years, his initial ₹15,000 SIP had automatically grown to over ₹45,000/month. Because of this invisible automation, his projected retirement corpus was nearly 40% larger than that of his peers who earned the same salary but kept their SIPs flat.

How to Psychologically Execute a Step-Up

If a 10% annual jump feels too aggressive, start with 5%. The exact percentage doesn't matter as much as the act of breaking the "flatline" mindset.

To understand the basics of mutual funds, they are long-term engines. A Step-Up SIP ensures you are feeding the engine the proper amount of fuel as your capacity grows, rather than running a Ferrari on a scooter's gas tank.

The Ultimate Wealth Multiplier

A flat SIP protects you from market volatility. A Step-Up SIP protects you from your own behavioral biases.

When you combine the mathematical power of Rupee Cost Averaging with the exponential power of a Step-Up mandate, you stop treating investing as a monthly chore and start treating it as an automated wealth-building architecture.

Stop telling yourself you will invest more "when you make more money." Automate the increase, and let the math do the heavy lifting.

Disclaimer

Mutual fund investments are subject to market risks. Read all scheme-related documents carefully. Please consult a certified financial advisor before making any investment decisions.

Trust & Compliance

This article has been created following our strict Editorial Policy. We believe in complete transparency regarding how we operate; you can read our Disclosures. For legal liabilities and risk factors, please review our Disclaimer.

Share & Save Article

Other Posts

What is Portfolio at Risk? A Complete Guide to Meaning, Formula, Calculation, & Benefits.

Jun 5, 2026

What is SIP & How Does It Actually Work?

May 27, 2026

What is an AMC in Mutual Funds? Understanding Asset Management Companies

May 27, 2026

How PMS Works: A Complete Guide to Construction, Monitoring, and Reporting

May 27, 2026